Editor’s note: This article is part of a larger report, Healthcare’s $1 Trillion Challenge, which provides a roadmap for creating a more affordable and sustainable healthcare system. In this article, we offer solutions for generating $640 billion in savings over 10 years by reimagining clinical work. Discover more chapters on relieving administrative burden and curbing the impact of growing drug costs.

Clinical labor spending is projected to double by 2035 to nearly $3 trillion. This is driven in part by the increase in demand for clinicians — demand for licensed practical nurses (LPNs), for example, is expected to increase by 20% from 2023 to 2035. Stagnant clinician productivity is another driver: From 1993 to 2021, hospital labor productivity grew only 0.2% per year. Data suggests that labor cost growth has regularly outpaced hospital volume growth since before the pandemic. The heavy reliance on high-cost sites like hospital campuses instead of alternative sites of care reinforces many of these expensive labor structures. Workflows suffer from inefficiencies that limit productivity and prioritize the wrong tasks. Even the most basic care interactions, such as taking a strep test or getting blood drawn, frequently involve multiple touchpoints.

Across the industry, stakeholders and innovators are keenly aware of these trends and reimagining the way they deliver care, but their impact has been isolated. The industry needs to scale these efforts and maximize their potential. Three levers will unlock $640 trillion in savings by 2035.

Optimizing care delivery to achieve $300 billion savings

Innovations in care delivery outside the walls of the hospital have been a major feature of the healthcare industry since 1970, when the first ambulatory surgical center (ASC) opened in Arizona. The industry has made progress investing in and expanding access to new sites of care, but gaps remain. Stakeholders need to renew their commitment to delivering care in the right place and at the right time to realize significant savings.

Reducing healthcare costs by moving hospitals to ambulatory care

Ambulatory surgery centers have long been recognized as high-quality, lower-cost sites for surgical procedures — a Medicare patient’s hip replacement in an ASC saves $3,000 in facility fees on one procedure. Many routine, low-complexity procedures like cataract removal and colonoscopies are done in ASCs today. Still, only about 20% of the total spending associated with ASC-eligible procedures occurs in an ASC today. For example, hernia repair procedures can be safely done without an overnight patient stay, yet a majority are still performed on a hospital campus, adding around $400 million in unnecessary spending per year.

To a certain extent, federal and state policies present barriers. The Centers for Medicare and Medicaid Services (CMS) in 2022 restored a list of nearly 300 procedures that it would only cover on an inpatient basis. Further, state certificate of need laws restrict the growth and development of ASCs. At the same time, a growing number of payers are investing in ASCs, standalone infusion centers, and other sites of care. Institutions that lead the shift to ambulatory sites of care will be increasingly rewarded with volume and profitability in a high-pressure cost environment.

Hospitals should recognize their ability to build ASCs that leverage their ability to handle complex cases.

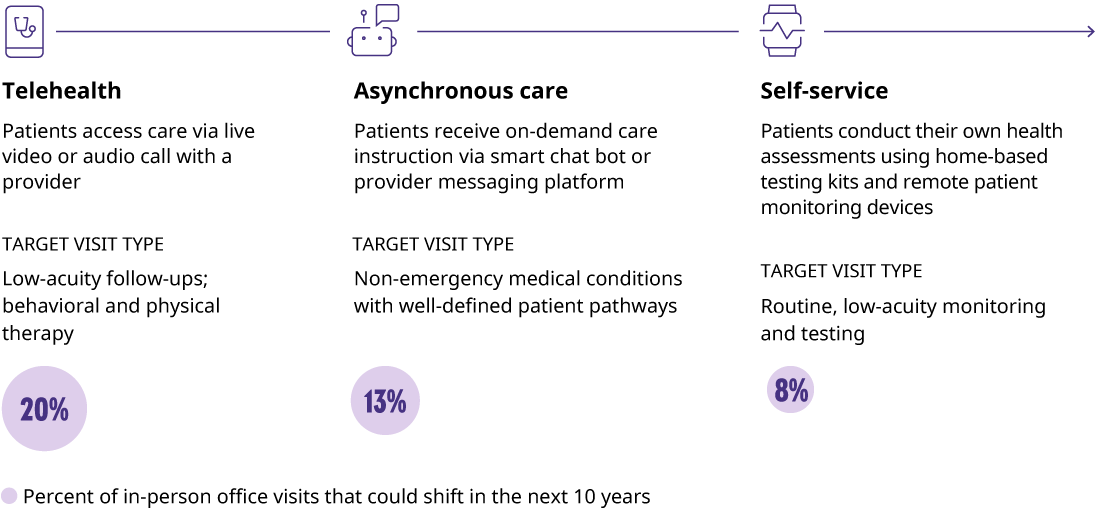

Saving costs with telehealth, asynchronous, and self-service solutions

The pressures of the pandemic resulted in accelerated investment and improvements in telehealth capabilities, asynchronous care platforms, and self-service solutions. Although telehealth use has declined from peak levels during the pandemic, visits remain an attractive alternative. Studies have found that unit costs are nearly 25% lower for telehealth visits than in-person visits, largely driven by lower labor and equipment needs. In addition, patients appreciate that telehealth appointments are typically less expensive, more convenient, and offer an opportunity to connect with expertise that is difficult to find locally. Continuing to push the boundaries on where telehealth can effectively deliver positive outcomes and working to expand user demographics will be imperative to ensuring telehealth can provide its full value in the healthcare system.

Asynchronous care delivery, including texting and messaging with care teams, has become increasingly accessible in recent years. Patient portals have integrated messaging features, and multiple new digital health startups are building platforms where users can message with a virtual care team for support. Asynchronous care delivery is more time-efficient, requires limited administrative coordination, and can prevent unnecessary visits to hospitals or urgent care centers. We estimate that nearly 60% of office visit costs are removed when replaced with asynchronous care delivery. Savings here can have major implications on the 2035 cost structure.

For many, COVID-19 home testing kits were their first interaction with self-service care. The concept is not new though — pregnancy tests, drug tests, and glucose meters have been used for years. Consumer-facing technology, including wearable and non-invasive devices, offer new potential for self-service care.

In one study, equipping coronary artery disease patients with a self-management care app, an Apple Watch, and a blood pressure cuff reduced readmission rates and saved institutions as much as $6,000 per patient. As these technologies become less expensive and easier to use, the potential of self-service care will reach new levels in 2035.

Saving $300 billion by shifting healthcare to home care

Home care is the next frontier in the migration of care out of the inpatient facility. Beyond home health and home hospice, a patient’s home is increasingly becoming an appropriate site to handle more complex episodes, like chronic obstructive pulmonary disease and cellulitis. We previously estimated that a sizable portion of inpatient admissions could be effectively delivered at home by 2035. After adjusting for patient complexity and social factors, it’s reasonable to expect roughly 40% of total inpatient care would be eligible to move to the home in 10 years.

That shift could enable significant savings. A recent study at Brigham and Women’s Hospital identified 38% savings when delivering care in a patient’s home compared to an inpatient stay, driven in part by fewer labs and imaging orders, as well as by fewer 30-day readmissions. Systems can also benefit from the downstream implications of opened capacity, like avoiding capital outlays to build, renovate, and maintain new hospital towers. All in, this can equate to over $2 million in savings per bed.

The barriers to home care are numerous and many programs have struggled to scale. Care at home operations and logistics differ significantly from facility-based care models, so upfront investment costs to build a new operating model, logistics networks, and a field workforce can be significant. To encourage this shift, payers will need to collaborate with their provider partners to develop a sustainable and attractive reimbursement model.

Care will be available through a wider variety of mechanisms in 2035, often in more cost-efficient and convenient ways. Shifting care to these optimal settings has the potential to take out over $300 billion in costs in 2035. The most effective future, though, will be one in which care is balanced across all sites, both legacy and new. Continuing to push boundaries, invest in innovative, multimodal offerings, and expand access will be key to realizing future value.

Improve care and save $60 billion by optimizing clinician roles

Allowing clinicians to practice to the top of their license is an oft-stated goal, but applied sporadically. Inconsistent scope of practice regulations limiting the services that nurse practitioners, physician assistants, and pharmacists can perform are a major factor. But the industry’s inverted talent pool also reinforces the challenges: There are more primary care physicians (PCPs) than advanced practice providers (APPs), and more registered nurses than certified nursing assistants.

Finding ways to grow the base of non-physician professionals and leveraging their expertise will allow physician practices to grow their panel sizes, decrease costs per encounter, and, in many cases, improve the quality of care. Increasing APP to PCP ratios from an average of 0.5 to 1 to 2.5 to 1 in primary care practices could improve productivity and boost panel sizes by over 600 patients. Extending this ratio to all primary care providers could save practices nearly $60 billion in labor spend in 2035. As physicians and nurses become increasingly more difficult to recruit, redesigning care practices will be integral to ensuring continued access for our patients.

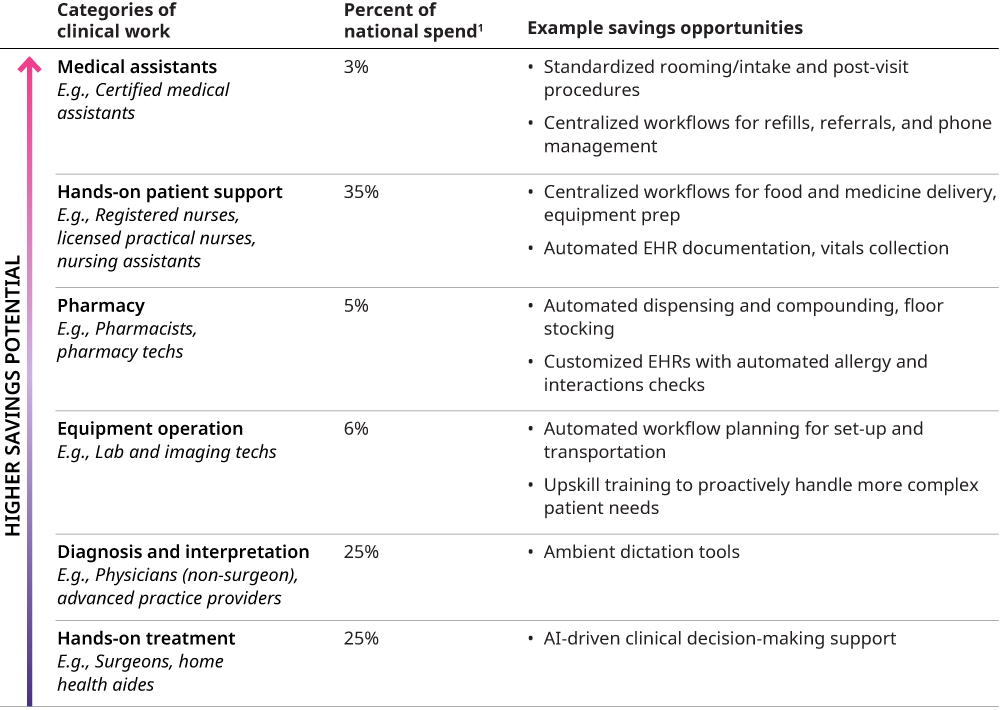

Three key strategies to save $270 billion by reimagining clinical work

Additional savings can be achieved by deconstructing current clinical roles into discrete tasks and redesigning roles and processes to make resources more efficient. Providers can enhance productivity across many clinical roles by standardizing processes, centralizing responsibilities, and automating repetitive workflows.

Boosting medical assistant productivity by 40% with key innovations

Our sister company Mercer found that 40% increased productivity among medical assistants in an ambulatory setting could be realized with standardization, centralization, and automation. For example, centralizing referral and medication refill management, standardizing rooming/intake forms by specialty, and automating data collection via e-check-in can maximize the organizational value of a medical assistant.

Optimizing nursing roles to improve efficiency and reduce workloads

Similar principles can be applied to RNs, nursing assistants, and orderlies, who account for more than one-third of the healthcare workforce. Studies report that nurses spend up to 41% of their time in the electronic health record (EHR) doing documentation and other tasks. Automating documentation and vitals collection can enable nurses to be upskilled for more complex tasks. LPNs can be trained to conduct basic lab tests or treat more complex wounds, reducing the burden on RNs. Centralizing straightforward tasks like food and medication delivery will further improve workforce efficiency.

Reimagining pharmacy roles and automation for major cost savings

The role of institutional pharmacists and pharmacy techs is becoming more critical, especially as the pipeline of specialty drugs expands and adds another layer of complexity to their work. Implementing tools to automate dispensing and compounding, incorporating overnight cart fill workflows and modern pharmacy robotics for automated floor stocking, can reduce staffing burdens. Customizing EHRs to automate drug interaction and allergy checks can relieve a significant portion of time for these resources. This creates time for more complex tasks without requiring additional resources and allows pharmacy professionals to focus on value-added functions.

Investing time to be intentional about reimagining how work is organized and how labor is best applied to these roles can save health systems and specialist physician offices over 10% in clinical labor costs, or just over $270 billion in 2035.

These three levers are tangible extensions of programs in place in organizations across the country today. Taken together, they could reduce clinical labor expenses by 25%, or $640 billion, and relieve significant pressure on the workforce.

And these levers could be applied in additional ways, such as expanding the use of APPs to specialty care practices, moving more care modalities — skilled nursing, urgent care — to the home, or implementing advancing technology capabilities like generative artificial intelligence (AI) to daily workflows to enhance job satisfaction and productivity. Care pathways themselves can be reimagined with expanding use of innovative AI tools in clinical settings. There is already momentum here: Ambient dictation is transforming provider-patient interactions, surgeries are being performed by doctors who are thousands of miles away from their patients, and doctors at Mass General Brigham are developing AI that can automatically administer anesthesia to C-section patients. Continuing to push the boundaries on how care can be delivered is imperative to achieving a more efficient labor cost base.

Removing structural barriers to achieve greater healthcare savings

Opportunities exist to create greater underlying change. Realizing the promise of even more radical savings will require alignment and support across the regulatory landscape. The practice of medicine is highly regulated across a patchwork of state and federal laws. Various professional associations define standards and boundaries of care, which are encouraged but not enforced. Standardizing and expanding the scope of practice laws across the country could motivate more people to pursue non-physician careers, which in turn generates momentum to use APPs and others across primary care and specialty practices. Streamlining federal standards and processes for reviewing and implementing technology into clinical processes would encourage the adoption of tools that make care safer and more affordable.

Building a more effective healthcare labor model by 2035

Better, more affordable healthcare with optimized care delivery

Site-of-care optimization practices will be standard across provider institutions, and consumers will receive care in more comfortable, more convenient, and more affordable settings. As lower-complexity cases move out of the hospital, wait times for critical patient care will be reduced. Boosted by support from APPs, physicians will have more capacity to see patients who won’t need to wait months for an appointment. Patients will have fewer low-value interactions with clinicians as advanced machines take over vitals collection and improved documentation methods streamline symptom logging and interpretation.

Creating efficient and satisfying roles for healthcare providers

More intentionally distributing patients across sites of care will ease pressures on overworked hospital staff. Practicing top of license will be the standard, not the exception. Institutions will invest more in retention and well-being programs as demand for labor begins to more closely mirror the supply pipeline.